The un-audited financial results of the three largest listed Lebanese banks (BLOM, Audi, and Byblos) for 2016 show that they have maintained their sustainable profitability, despite the continuing difficult operating conditions arising from the political and economic turmoil in Lebanon and in neighboring countries. Aggregate net profit increased to $252.17 million in the first quarter of 2016, growing by 12.59% over the same period in 2015. This increase in net profit was largely obtained as a result of the increase in profits of the banks’ units outside Lebanon.

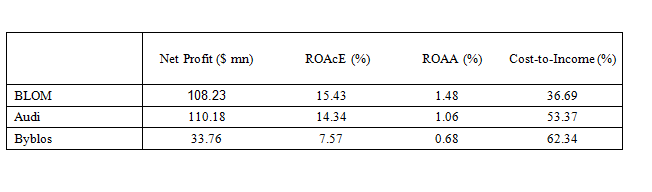

On an individual basis, Bank Audi reported the highest net profit of $110.18 million, growing by 10.15% from the first three months of 2015. BLOM Bank came second, growing its net profit by 18.71% to reach $108.23 million; while Byblos Bank’s net profit ranked third, growing by 3.05% to $33.76 million.

The profit performance of the three banks can also be seen from looking at profitability ratios, namely the rate of return on average common equity (ROAcE) and on average assets (ROAA), which measure the productivity to generate earnings from equity and assets. BLOM Bank recorded the highest ROAcE at 15.43% and the highest ROAA at 1.48%. The two other banks followed, with Bank Audi’s ROAcE at 14.34% and ROAA at 1.06%, and Byblos bank’s ROAcE at 7.57% and ROAA at 0.68%. BLOM bank’s high profitability ratios can be attributed to its superior managerial and operational efficiency. This is demonstrated by BLOM bank’s cost-to-income ratio of 36.69%, the lowest of all three, followed by 53.37% for Bank Audi and 62.34% for Byblos Bank[1].

Growth was not limited to profit only, since it was also registered in key balance sheet items. BLOM reported $29.3 billion in assets, growing by 4.31% from end of March 2015, while its loan portfolio grew by 5.27% to $7.28 billion and its shareholder’s equity went up by 7.72% to $2.79 billion. Assets at Byblos reached $20.05 billion, growing at 5.73%, while its loan portfolio increased by 4.15% to $4.88 billion, and its shareholder’s equity rose to $1.74 billion at a rate of 2.07%. As for Audi, its assets fell by 1.05% to $41.02 billion, with its loan portfolio increasing by 10.08% to $18.1 billion, while its shareholder’s equity fell by 0.59% to $3.36 billion.

As important, the three banks’ performance also involved strong banking fundamentals. In this respect, for all three banks, net non-performing loans ratios did not exceed 1.5% (Audi, 0.9%; Byblos, 1.2%; BLOM, 1.5%), capital adequacy ratios did not go below 13.7% (BLOM, 18%; Byblos, 17.3%; Audi, 13.7%), and primary liquidity ratios did not fall below 44.4% as well (BLOM, 66%; Byblos, 52%; Audi, 44.4%).

Once again, these results show the top three listed Lebanese banks’ ability to maintain good profitability and financial strength by pursuing conservative and cautious policies, given the exceptional circumstances still facing them. As a result, they reconfirm the Lebanese banking sector’s position as the leading financial pillar in the country and the backbone of the economy.

[1] The cost-to-income ratio excludes depreciation.