The resolution of an 18-month long dispute between Egypt and Qatar, which was brokered by Saudi Arabia, did not last very long as an Egyptian official accused Qatar of financing terrorism, a list that has included both the Islamic State in Syria and Iraq, and Hamas in Palestine.

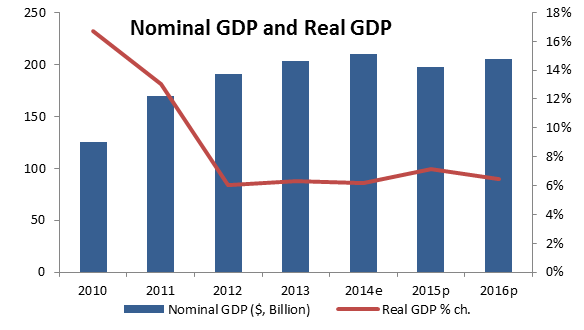

The undergone projects in preparation for the FIFA World Cup 2020 resulted in a 6.7% year-on-year (y-o-y) growth in Qatar’s real GDP, in the last quarter (Q4) of 2014. Qatar plans on making at least 80% of all development projects related to the event to be sustainable and available for use after 2020.

Real Gross Value Added (GVA) of the non-oil sector, with a 62.84% share of GDP, posted a 10.3% yearly growth in Q4 enhanced by double-digit upsurges witnessed in electricity, construction, trade, hotels, transport & communication, and domestic services. Major infrastructure and construction projects, which are mainly expected to be finalized before the FIFA World Cup 2020, led to a 17.7% y-o-y development in construction activity. Similarly, the GVA of the oil and gas sector grew by only 1.3% y-o-y as the halt on further gas explorations on the North Field is being implemented.

Inflation was contained at 1.4% y-o-y in March 2015, mainly affected by 4.1% and 6.1% price rises in “Housing , Water, Electricity & Gas” (21.89% weight) and “Transport” (14.59%). It is worth noting that the CPI was calculated using new weights and with 2013 as a base year.

On the suppliers’ side, the Producer Price Index (PPI), measuring the average selling prices domestic producers receive for their output, plunged by 41.4% y-o-y in January, primarily due to the sharp decline in prices of crude oil and natural gas during 2014. The price of the Qatari Land Crude Oil (QLCO) and that of the Qatari Marine Crude Oil (QMCO) shed from $76.2/barrel and $74.4/barrel end of November 2014, to $56.1/barrel and $53.5/barrel end of February 2015. Therefore, the “Mining” group, which represents 77% of the PPI plummeted 44.3%. The PPI subcomponents of “Manufacturing” activity and “Electricity and water” activity also showed yearly drops of 31.7% and 1.7%, respectively.

Looking at the country’s external position, Qatar’s trade balance, plunged by 47.87% y-o-y to $9.92B by end February 2015, arising from lower exports and higher imports. Declining oil prices drove down the largest component of total exports, hydrocarbons, by 44.84%, causing a 36.36% y-o-y plummet in exports to $15.05B by February 2015. On the other hand, imports increased by 10.93% y-o-y to $5.12B, where motor cars and other passenger vehicles were the top imported commodities, rising by a yearly 20.86%.

On the fiscal front, Qatar’s budget surplus is expected to narrow from 10.8% of GDP in 2014 to 8% in 2015. Revenue growth is projected to drop from 46.9% of GDP to 40% in 2015, due to the impact of lower energy prices on hydrocarbon revenues (representing 55% of total state revenues). However, receipts from corporate income tax collection and transfers from state-owned companies are expected to partly offset the decline in hydrocarbon revenues. Expenditure is expected to stand at 32% of GDP, mirroring a forecasted 45.8% increase in capital spending.

Looking at the monetary sector, total assets at commercial banks dipped 1.29% since 2014 to $267.78B, by February 2015. Public sector credit dropped 5.71% since year start to $59.46B by February, while that of the private sector edged up 1.55% to $96.78B. Total deposits showed a marginal 0.16% growth to $162.55B, due to the 0.95% and 1.07% decreases in public deposits and resident private sector deposits that partly offset the 13.74% growth in non-resident deposits.

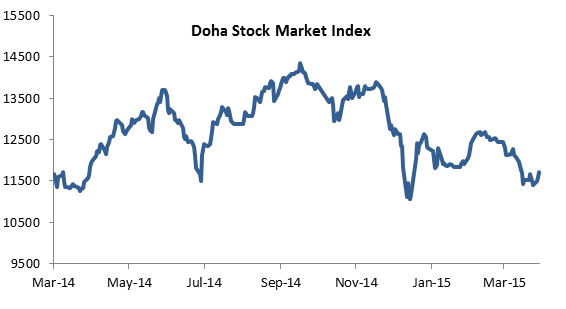

Falling oil prices continued to impact investor’s sentiment, where the Doha Stock Market Index (DSMI) inched up slightly by 1.30% q-o-q to 12,445.30 points end of March 2015. Trade during the first quarter of 2015 occurred at a lower volume of 716.28M shares worth $8.30B compared to 880.56M shares worth $12.45B during Q4, 2014.