While other Arab countries were struggling to stop the flow of blood on their land, the United Arab Emirates (UAE) was setting for its space exploration of the red planet Mars. Other megaprojects and large-scale schemes were also planned by the end of 2014 with Dubai outpacing the region by 20 years in terms of shopping and retail, through the Mall of the World. As a matter of fact, the expected mall which will be the largest in the world, will also record another milestone as it will be the first “temperature controlled city” globally.

While other Arab countries were struggling to stop the flow of blood on their land, the United Arab Emirates (UAE) was setting for its space exploration of the red planet Mars. Other megaprojects and large-scale schemes were also planned by the end of 2014 with Dubai outpacing the region by 20 years in terms of shopping and retail, through the Mall of the World. As a matter of fact, the expected mall which will be the largest in the world, will also record another milestone as it will be the first “temperature controlled city” globally.

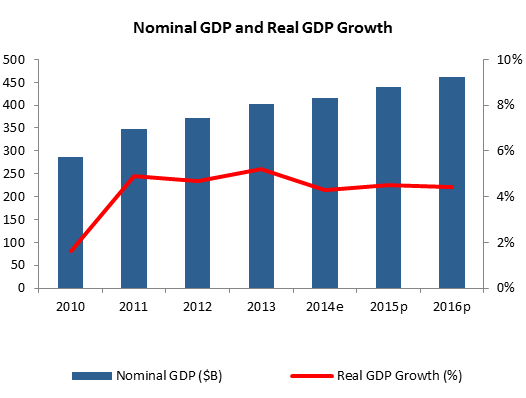

Targeting a full recovery since 2009’s crisis, the UAE’s authorities insisted on boosting infrastructure, tourism and real estate projects which secured a solid economic growth over the past 5 years. The International Monetary Fund (IMF) estimated economic growth to stand at 4.3% by the end of 2014 and to reach 4.5% by 2015. In the same context, the UAE’s Purchasing Managers’ Index (PMI), which mirrors the performance of the non-oil producing private sector, improved to 58.4 in December 2014 compared to 57.4 a year ago, which indicates an accelerating economic activity. The average inflation rate in Dubai reached 3.36% in 2014 after standing at 1.31% a year earlier following upticks in the prices of rents, food items and education costs. As for the Emirate of Abu Dhabi, the average inflation rate for 2014 stood at 3.23% following a slight 0.24% inflation in 2013. The increase in Abu Dhabi’s general prices in 2014 can be primarily attributed to the rise in the “Housing, water, electricity, gas and other fuels” group.

The tourism industry in Dubai maintained its steady growth during the last quarter of 2014 with Dubai International airport overtaking London’s Heathrow airport and becoming the world’s busiest hub in the world. The former saw the number of passengers reach a record level of 70.48M in 2014, 6.1% higher than 2013’s level. Moreover, Dubai hotels maintained their top ranking amongst the Middle East and North Africa (MENA) countries in terms of occupancy rate at 79% by November 2014, barely inching down by one percentage point from the same period of 2013. Abu Dhabi ranked second with a 78% hotel occupancy rate, one percentage point higher than that of the first eleven months of 2013.

The Emirates external position mirrored in the fourth quarter of 2014 the substantial international oil prices decline. Thus, and while UAE’s current account is expected to narrow by a yearly 21.4% to $48.5B in 2014, UAE’s trade surplus is projected to tighten by a yearly 8.1% to $113.1B over the same period. This resulted from a 3.03% y-o-y increase in total imports versus a 0.71% annual drop in total exports (hydrocarbon and non-hydrocarbon exports). In this context, the falling energy prices are expected to have triggered down hydrocarbon exports by 10.2% in 2014 to $108.7B which will outpace the estimated 4.0% y-o-y increase in non-hydrocarbon exports to $256.0B.

In line with the bearish oil prices trend that marked 2014, UAE’s fiscal performance was also heavily impacted despite its ongoing diversification strategy away from oil. In details, the consolidated fiscal balance is expected to narrow in 2014 by 30.3% y-o-y to stand at $31.50B, if net lending was excluded from expenditures. As for the consolidated government expenditures (excluding net lending), estimates stood at $101.41B or 24.6% of 2014’s GDP, up by 5.0% from 2013’s level. Consolidated revenues are forecasted to drop 6.3% y-o-y to $132.92B or 32.3% of GDP following a 10.0% yearly decrease in hydrocarbon revenue (that almost constitutes 75.6% of total consolidated revenues).

Regardless of the decrease in revenues resulting from the tumbling oil prices, Emirati authorities are not planning to impose any additional taxes in 2015 to compensate for the losses occurred. Similarly, and without any modification, the UAE’s 2015 federal budget was approved by the Federal National Council in December amounting for $13.37B (A 6.3% rise from 2014’s budget). The UAE’s sovereign wealth fund buffers and the relatively lower fiscal breakeven price compared to other major oil producers will probably sustain oil prices from triggering growth down. On the brighter side, Dubai managed to pass, in the beginning of 2015, its first deficit-free budget since the crisis amounting for $11.16B.

Monetary developments mirrored the strong economic growth. In fact, M3 widened 11.3% from December 2013 to reach the $369.66B by the end of November 2014. Total bank assets rose to $637.76B in the first eleven months of 2014, up from $561.51B recorded in November 2013. Investors’ confidence and the overall positive sentiment in the country were the main drivers of lending activity with total bank loans and advances rising by 10.2% y-o-y to $380.57B by November 2014. Likewise, total deposits increased by a yearly 12.3% to settle at $388.22B over the same period.

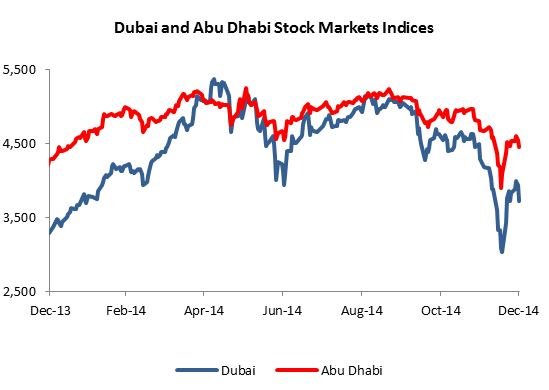

Despite a frailer trading, Dubai and Abu Dhabi bourses ended 2014 in the green. The former’s stock index edged up by 12.0% y-o-y to 3,774.0 points, while Abu Dhabi’s index posted a 5.6% uptick to 4,528.93 points. Accordingly, Dubai’s market capitalization broadened by an annualized 28.1% to $85.63B by December 2014, while that of Abu Dhabi widened by 3.3% y-o-y to $113.71B.

On Dubai’s stock market, the average daily traded volume narrowed by 35.4% y-o-y to 445.54M shares in Q4 2014 at an average traded value of $286.90M (compared to an average value of $239.80M in Q4 2013). The number of transactions retreated to 499,670 over the same period, down from 561,952 recorded a year earlier.

In Abu Dhabi, the average daily volume traded tumbled to 153.95M shares worth $90.08M in Q4 2014 compared to 286.25M shares valued at $129.93M recorded a year earlier. As for the number of transactions, it reached 161,217 in Q4 2014, slightly below 2013’s same quarter level of 168,081.