The third quarter of 2015 proved to be a very difficult period to navigate through, as global financial markets experienced volatility hardly seen before, and economies witnessed withdrawals and stagnations on the back of economic and financial developments in Asia and Europe primarily. The Hashemite Kingdom continued to benefit from cheaper energy prices and took the appropriate measures to protect itself from the worsening economic situation.

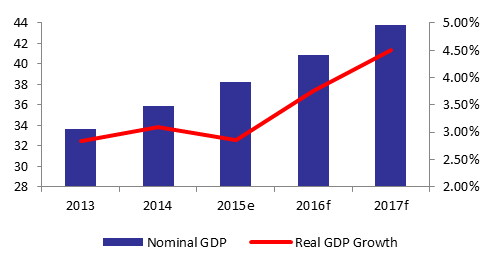

As global projections for GDP growth diminished, International Monetary Fund (IMF) forecasts for 2015 GDP growth were revised to 2.85% from a previous forecast of 3.80% and nominal GDP for the year is expected to stand at $38.21B (JOD 27.10B). In addition, Jordan’s Consumer Price Index (CPI) witnessed a 1.18% y-o-y decrease to 116.81 points. The continuing deterioration of the global economic situation and regional security threats largely contributed to the poor performance of Jordan’s tourism sector throughout the year. As of June 2015, the total number of tourists had registered a 15.42% annual decrease to 2.32M tourists. The Ernst & Young hotel occupancy report indicated that the capital, Amman, revealed a 9 percentage-point decrease in the occupancy rate to 54% by August 2015 in comparison to the same period last year. Similarly, average room rates and room yields in Amman decreased annually by 6.06% and 18.27% by August to respective values of $155 and $85. In parallel, travel receipts during the first seven months of 2015 lost 11% y-o-y to reach $1.13B. Despite the deficit in the Kingdom’s Current Account narrowing by a yearly 3.03% to $1.60B (JOD 1.14B) by end-June on the back of cheap oil, Jordan’s Capital & Financial Account displayed an 18.13% annual decline over the same period to $791.86M (JOD 561.60M). This resulted in an 18.33% y-o-y widening of the country’s Balance of Payments deficit to $809.20M (JOD 573.90M) during the first six months of 2015. The performance of Jordan’s trade sector, on the contrary, showed notable improvements. The Kingdom is a net importer, especially regarding commodities, and therefore greatly benefited from the bearish trend of prices for energy and metals. During the first seven months of 2015, Jordan’s trade deficit experienced a 15.66% contraction to $7.06B (JOD 5.01B) compared to the same period in 2014. This improvement came about as a result of the 12.49% decline in imports to $11.54B (JOD 8.19B), which outweighed the 6.97% yearly decrease in total exports (which include re-exports) to $4.48B (JOD 3.18B). The retreat in the value of imports can be directly linked to the low oil prices witnessed throughout 2015. In details, the value of imports of petroleum crude and gas oil/diesel fell by 36.14% and 64.68% to respective values of $887.76M (JOD 629.61M) and $496.82M (JOD 352.35M), respectively, by July 2015. Imports of cereals also lost 32.18% of their value to $229.33M (JOD 212.29M) over the same period. Regarding exports, the most noteworthy developments were the increase in knitted and crocheted apparel and clothing as of July 2015 by 10.29% y-o-y to $751.21M (JOD 532.77M). In contrast, exports of mineral and chemical fertilizers lost 22.88% to $234.10M (JOD 166.03M). Despite the Kingdom’s fiscal surplus in the first quarter of 2015, Jordan recognized a fiscal deficit of 315.14M (JOD 223.5M) by June 2015, inclusive of foreign grants that reached $417.92M (JOD 589.27M). During the same period in 2014, the fiscal deficit recorded $499.28M (JOD 354.10M). Net outstanding public debt rose by 4.04% y-o-y to $30.16B (JOD 21.39B), and accounted for 78.80% of GDP by June 2015, compared to 80.80% during the same period in 2014. In details, outstanding external public debt increased by $1.49B (JOD 1.06B) between the first six months of 2014 and 2015 to attain $12.82B (JOD 9.09B), equivalent to 33.50% of GDP, while outstanding domestic public debt decreased by $321.48M (JOD 228M) to $17.34B (JOD 12.30B), equivalent to 45.30% of GDP. Developments in the Kingdom’s monetary sector included a 6.25% y-t-d uptick in money supply M2 to $43.81B during the first seven months of 2015. As of July 2015, licensed banks had extended an additional 5.20% of credit facilities y-o-y, for a total of $28.60B (JOD 20.29B). Over the same period, total deposits at licensed banks gained 5.70% during the year to $45.09B (JOD 31.98B). Meanwhile, foreign currency reserves at the Central Bank of Jordan experienced an $862.9M rise by end-July to stand at $14.94B. This level accounts for roughly 7.8 months of the Kingdom’s imports. In a bid to spur economic spending and investment sentiment, the Central Bank of Jordan (CBJ) lowered interest rates by a further 25 bps on July 9th, resulting in y-t-d decreases of 50 bps on the re-discount rate and the overnight repo rate to 3.75% and 3.50%, respectively. The main interest rate now stands at 2.50%. The performance of the Amman Stock Exchange was reflective of the global equity market, as the ASE lost 3.93% by end-September. The bourse ended the third quarter at 2,080.41 points, with a market cap of $24.33B (JOD 17.25B), compared to $25.70B by September 2014. However, we notice a increasing trend in the number of shares traded and their values by 21.12% and 41.01% to 2.04B shares worth $3.39B (JOD 2.41B), indicating the existence of a bearish market.