Similarly to the previous years, the United Arab Emirates (UAE) held on to its strategic goals despite the global economic headwinds and the escalating regional tensions. Deteriorating oil prices were another reason for the UAE to persevere in its diversification scheme away from hydrocarbons. This was highlighted by the approval of $35B government investment plan during the last quarter of 2015 to target a lower dependence on natural gas for electricity production from a 100% to a 70% level by 2021. Furthermore, an equally financed strategic investment fund worth $10B was established between the UAE and China during Q4 2015. The 3-Year agreement will strengthen the political and economic cooperation between the two countries, noting that China is pursuing to rebuild the “Silk Road” trade route that connects the Asian country to the Mediterranean countries. The UAE pursued their ambition to become a knowledge-based economy through several measures in Q4 2015 such as the $81.7B investment that includes 100 initiatives in education, transportation, health and water. The quarter was also marked by the opening of the first overseas branch of the Egyptian-based Al Azhar University in the UAE.

On a different front, the Emirates kept on supporting the war-riddled Arab countries like Libya and Yemen through humanitarian and military provisions. Locally, 20 new members were elected to the Federal National Council, the UAE’s government advisory body.

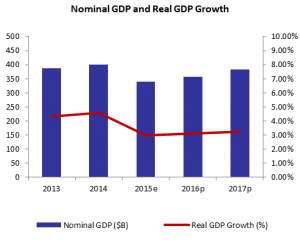

The slowing economic growth in the UAE, which was emphasized by the slackening Gross Domestic Product (GDP), mostly reflected the bearish trend of global oil prices. In reality, the International Monetary Fund (IMF) has estimated the real GDP growth to have reached 3% in 2015, down from a previous 4.57% in 2014. This came on the back of the 37.2% yearly fall in international oil prices in 2015. In another context, the non-oil private sector in the UAE also reflected a slowing growth as the Purchasing Managers’ Index (PMI), declined from an average 59.3 in Q4 2014 to 53.9 in Q4 2015. Still, the index signaled continuing economic expansion, even if at a slower pace, mainly on the back of slower rises in output, new work, and employment. When it comes to prices in the UAE, the slump in oil prices was more than offset by hikes mostly in “Housing and utility costs”, “Furniture and Household Goods” and “Education” prices. Inflation rate in Dubai more than doubled in Q4 2015 as it reached 3.2% compared to a lower 1.5% in Q4 2014. In Abu Dhabi, inflation in Q4 2015 stood at 6.1%, up from 3.89% in Q4 2014, which mostly resulted from the Emirate increasing electricity and water tariffs in January.

Tourism in the Emirates seemed to have maintained its momentum, while hospitality saw slowing activity in 2015. For the second year in a row, Dubai International Airport (DXB) maintained its title as the world’s busiest airport recording a 10.7% yearly rise to 78.01M passengers. According to Network International, tourist spending saw yearly improvement in the third quarter of 2015 after 2 quarters of declines. The improvement was derived from the progressing spending levels of the top 3 overall spenders in Q3 2015 compared to the previous quarter: United States (+15%), Saudi Arabia (+29%) and United Kingdom (+17%). However, the earlier drops in the past 2 quarters of 2015 were mainly linked to the dropping numbers of Russian (-57%) and Chinese (-20%) tourists, which probably resulted from the depreciation of both the Ruble and Yuan during 2015.This also caused the hospitality industry to slow down despite the almost stagnating occupancy rates in the Emirati 4-and 5-stars hotels. In reality, Dubai’s hotel occupancy rate remained at 80% by December 2015, while that of Abu Dhabi slipped by 1 percentage point to 78%. Also, each of Dubai’s average room rate (AVR) and revenue per available room (RevPar) dropped by 6% to $259 and $208, respectively. In Abu Dhabi, the AVR shed 3% y-o-y to $170, while the RevPar lost 5% to $133.

The UAE external position was one of the economic aspects to most mirror the decline in global oil prices. The current account surplus is estimated to have significantly fallen from 13.6% of GDP in 2014 to 2.6% of GDP in 2015. Similarly, trade deficit tightened from an expected $130.4B in 2014 to $80.7B by the end of 2015. With total imports expected to slump by a yearly 4.5%, total exports are expected to decline at a faster pace of 16.3% y-o-y given the 45.0% drop in hydrocarbon exports. As a matter of fact, hydrocarbon exports constituted 19.8% of total exports in 2015 compared to a 30.1% stake in 2014, which emphasized the Emirates’ diversification strategy that was maintained amid lingering headwinds over decreasing oil prices. Grasping an 80.2% stake of total exports, non-hydrocarbon exports slipped 4.0% y-o-y in 2015.

The global economic dynamics also took their toll on the public finance of the UAE. In particular, the fiscal balance of the Emirates was heavily hit by the falling oil prices noting that hydrocarbon revenues tumbled by a yearly 40.4% in 2015, almost constituting 56% in 2015, down from a 68% share of total revenues in 2014. In this context, and for the first time since 2009, the UAE is expected to post a consolidated fiscal deficit near $14.54B (almost 4.5% of GDP) in 2015, down from a previous yearly surplus of $19.90B (almost 5% of GDP). According to the International Institute of Finance (IIF), this resulted from the 27.2% downturn in the Emirates consolidated revenues, compared to the 5.0% yearly slump in the consolidated expenditures (excluding net lending). Aiming to curb federal spending amid the cheap oil environment, the UAE approved a smaller federal budget for 2016 amounting to $13.2B with a zero fiscal deficit, slightly lower than 2015’s budget of $13.4B.

On the monetary front, the Emirati central bank announced the increase of interest rates on its certificates of deposits by 25 basis points (bps) in December in line with the Federal Reserve’s decision to increase interest rates by 25 bps for the first time in nine years.

However, banking activity maintained its momentum between September and December 2015. Despite the declining government deposits, money supply M3 managed to show further progress as it rose by 2.4% y-o-y to settle at $371.25B by the end of 2015.The Emirates’ total banks assets revealed a 6.1% yearly growth to reach $665.95B by December 2015. Moreover, lending activity also improved as domestic credit increased by an annual 8.1%, amounting to $376.26B in Q4 2015. In details, private sector loans (76% of total lending) progressed by 9.1% y-o-y, while those of the government showed a 9% improvement in 2015. Total deposits increased by 3.6% y-o-y to $400.77B by December 2015, as private sector deposits witnessed a 7.3% uptick in 2015 while government deposits dropped by 17.9% over the same period.

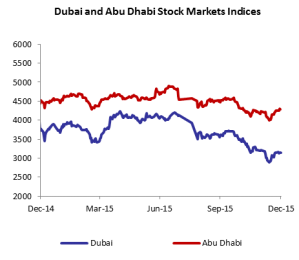

Investors’ uncertainty worsened during the last quarter of 2015, which was reflected on the Emirati stock markets. In particular, Dubai’s and Abu Dhabi’s bourses were negatively impacted by the tumbling oil and commodities’ prices, the Chinese economic slowdown and the expectations of higher interest rates in the United States. All of this is reflected by the indices of both Dubai and Abu Dhabi, which respectively lost 12.3% and 4.5% q-o-q to 3,151.00 points and 4,276.14 points by the end of December. Accordingly, Dubai’s and Abu Dhabi’s market capitalization narrowed from $88.97 and $115.65B by December 31, 2015 to $73.09B and $109.24B this year, respectively. In terms of trading activity, the average daily traded volume in Dubai narrowed by 11.2% q-o-q to 190.78M shares in Q4, 2015 compared to an average daily traded volume of 214.88M shares in Q3, 2015. Abu Dhabi experienced similar market dynamics, as the average daily volume fell by 15.9% q-o-q to 74.43M shares in Q4, 2015 compared to 88.51M shares in Q3, 2015.