2015 proved to be a very challenging year for the majority of global economies. However, while the Hashemite Kingdom was certainly affected in certain aspects, with the first six months proving to be especially difficult due to the compounded impact of local and regional concerns, Jordan did manage to protect its economy from more severe consequences. Improvement was mostly witnessed in trade, while the second half of 2015 saw Jordan recover from earlier drawbacks in most sectors.

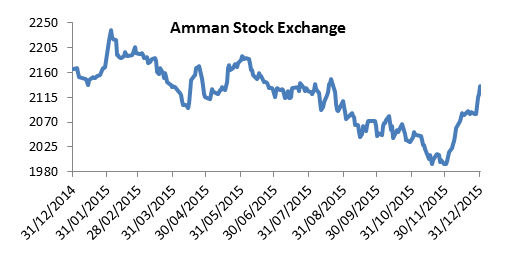

Following lower global growth expectations, the International Monetary Fund (IMF) estimated a real GDP growth of 2.85%, with an expected improvement to 3.75% and 4.50% by 2016 and 2017, respectively. The Kingdom’s 2015 nominal GDP is expected to reach $38.21B, growing to $40.89B and $43.82B in 2016 and 2017, respectively. Jordan’s tourism sector significantly improved from the poor performance witnessed over the first half of 2015 following poor global economic conditions and local security concerns. By the end of Q3 2015, the annual decrease in total tourists improved from 17% by June 2015 to 5.3% by end-September. This translated in to a total number of 3.78M visitors to the Kingdom, compared to 4.16M over the same period in 2014. The EY Middle East Hotel Benchmark Survey also indicated the drop in tourism activity, as the hotel occupancy rate over the entirety of 2015 decreased by 6 percentage points to 56%, while the average room rate and yield revealed respective annual downturns of 4.7% and 13.7% to $109 and $61, respectively. Jordan’s balance of payments (BoP) recorded a deficit of $936.24M (JOD 664M) over the first three quarters of 2015. The Current Account (CA) registered a deficit that widened by 36.80% y-o-y to $2.69B (JOD 1.90B) following a decrease in the surplus of net current transfers by $1.19B to (JOD 843.8M), while the capital and financial account registered a surplus of $1.75B (JOD 1.24B). The deflationary pressure on several commodities helped boost Jordan’s trade sector, as the Kingdom’s trade deficit over the first ten months of 2015 narrowed by 12.80% y-o-y to $10.51B (JOD 7.45B). Total exports, which include re-exports, decreased by 6.10% y-o-y by October to register $6.56B (JOD 4.65B) as exports of vegetables, and medical and pharmaceutical products, lost 8.90% and 4.90% to respective values of $488.14M (JOD 346.2) and $453.88M (JOD 321.90M). Meanwhile, exports of phosphates gained 11% to $426.53M, 68.83% of which was sold to India. Over the same period, total imports decreased by 10.30% to $17.06B (JOD 12.10B) on the back of significantly lower pricing of petroleum products and crude oil. The latters’ imports registered decreases of 59.9% and 40.7% to new levels of $1.23B (JOD 872.6M) and $1.17B (JOD 826.7M), respectively. Jordan’s fiscal deficit continued to widen, as the general budget (inclusive of foreign grants), recorded a deficit of $1.18B (JOD 835.6M) by October 2015. This is representative of a 20.06% expansion when compared to the same period in 2014. Total public revenues revealed a 5.48% decline over the first 10 months of the year to $7.46B (JOD 5.29B), mainly on the back of the 43.29% yearly slide in foreign grants over the period to $576.83M, in addition to reductions of general sales tax on certain items and special tax to 8% from 16% and 25%, respectively. In contrast, net outstanding public debt by October 2015 grew by 9.88% since the end of 2014 to stand at $31.85B (JOD 22.59B). Consequently, net outstanding public debt by October equaled 83.30% of GDP, compared to 80.80% by December 2014. Outstanding external public debt increased by 19.20% y-t-d by October 2015 to $13.50B (JOD 9.52B), or 35.30% of GDP. Outstanding domestic debt also rose by 3.90% y-t-d to $18.35B (JOD 13.01B), or 48% of GDP, over the same period. On the monetary front, the Central Bank’s foreign currency reserves ended 2015 at a level of $14.15B, compared to $14.08B a year earlier. These reserves are sufficient to cover an estimated 7.5 months of Jordan’s imports. In terms of domestic liquidity, the money supply M2 gained 8.09% over 2015 to stand at $44.78B (JOD 31.61B) as total credit facilities extended by licensed banks increased by 9.49% y-o-y to $29.90B (JOD 21.10B) over the same period. Meanwhile, total deposits at licensed banks jumped 7.72% annually to $46.19B (JOD 32.60B), driven by the rise in resident private sector deposits by 7.60% to $36.56B (JOD 25.80B) by December 2015. 79.80% of total deposits at licensed banks were denominated in the Jordanian currency by the end of the year, compared to 79.35% at the end of 2014. Interest rates remained stable since July 2015, with the re-discount rate and the overnight repo rate at 3.75% and 3.50%, respectively. Meanwhile, the interbank rate dropped from 3.00% in December 2014 to 2.08% by end-2015. The Amman Stock Exchange ended the year at a decrease of 1.35% from 2014’s close, following a flurry of foreign investments in listed securities during December. During the month, 75.8% of trading value on the Amman Stock Exchange represented non-Jordanian investment, contributing to net inflows of foreign investment of $14.95M (JOD 10.60M) during 2015. The ASE’s market capitalization decreased by 0.35% annually to $22.72B (JOD 16.11B). Total trading volume reached 1.65B shares, up from 1.42B the previous year. The value of total trades mirrored the increase in total trades, gaining $500M to $2.93B by end-2015.