Amid a continuing political stalemate, with around 21-month of political vacuum, most of Lebanon’s economic indicators recuperated from the low levels reached in the previous years. However, the geopolitical dynamics were not as smooth, as GCC countries (Bahrain, Kuwait, Qatar, and Saudi Arabia) warned their citizens from travelling to Lebanon. This occurred after Saudi Arabia halted $4B in aid to the Lebanese Armed Forces in response to diplomatic differences with the Lebanese government.

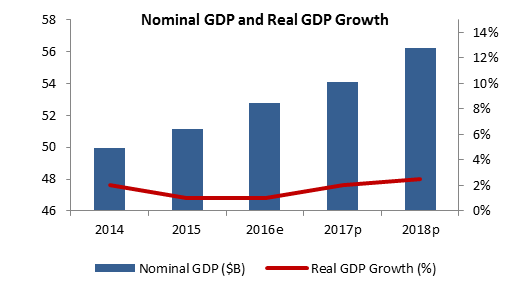

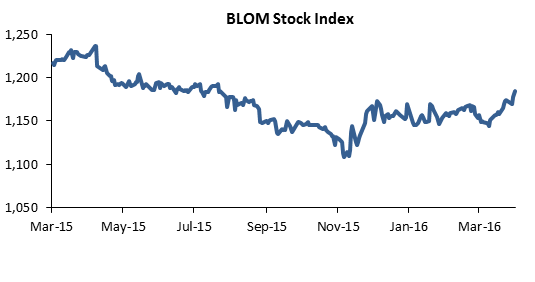

Due to the shaky political environment, the International Monetary Fund estimated Lebanon’s Real Gross Domestic Product for 2016 to grow at the same pace of 2015. The BLOM Purchasing Managers’ Index remained below the 50 mark, at an average of 47.2 points in the first quarter (Q1) of 2016, marginally lower than the 47.3 points registered in the previous quarter. Looking at consumer prices, they maintained their downward trend on the back of the persisting decline in oil prices, depreciating euro, and the global and local slowdown. Hence, the CPI decreased by 2.94% y-o-y to 94.25 points, in February 2016. “Food and non-alcoholic beverages” (20.6% of CPI), “transportation” (13.1% of CPI) and “water, electricity, gas & other fuels” (11.9% of CPI), witnessed yearly drops of 2.05%, 4.83% and 16.54%, respectively. Looking at the real-estate sector, total transactions (local and foreign) increased 14.5% annually to 19,640 worth $2.08B by Q1 2016. In details, land transactions posted a 19.37% y-o-y growth to 10,384 transactions, while build units increased by 9.55% to 9,256 transactions by Q1 2016. Average value of land transactions went up from $102,399 in Q1 2015 to $106,147 in Q1 2016. However, foreigners’ share of the total number of real estate transactions went down from 2.08% in Q1 2015 to 1.52% in Q1 2016. Similarly, construction improved after 4 years of frail activity. The number of permits reached 4,067 by February 2016, compared to 1,996 in the same period of 2015. Noting that permits are usually issued at least 6 months after applications are filed, the growth in construction activity could be partly attributed to contractors’ optimism regarding the upcoming year, and the improved security situation in the North. As for tourism, the number of incomers increased by 9% yearly to 191,808 by February 2016. Accordingly, hotel occupancy improved, with the average rate adding 2 percentage points to 55% by February. Nonetheless average room rate and average room yield lost 16.7% and 14.3% to $142 and $79, respectively, which could be the result of the type of tourists in light of the warnings issued by GCC countries and/or following the trend in the region. However, Global Blue’s Tourist Spending Report revealed that tourist spending in Lebanon declined 12% y-o-y in Q1 2016. Lebanon’s Balance of Payments revealed a deficit of $356.3M in the first two months of 2016, compared to a higher deficit of $432.8M in the same period last year. In spite of the relative improvement, the overall weakening in European and GCCs economies might be still weighing on the remittances and Foreign Direct Investments (FDIs) to Lebanon. In contrast, trade deficit widened from $2.17B by February 2015 to $2.46B by February 2016. Total imports grew 7.93%, while exports plunged 14.89% y-o-y in the first 2 months of 2016. Fiscal deficit broadened 28.62% yearly to $3.95B in 2015. Therefore primary surplus declined to $724M compared to a higher primary surplus of $1.34B, end of 2014. This was mainly driven by the 11.98% decline in total revenues exceeding the 3.04% drop in total expenditures. The drop in revenues resulted from the 4.34% decrease in VAT revenues, while the 45.81% plunge in EDL transfers was the main reasons behind the decline in expenditures. The deficit led Gross public debt (GPD) to stand at $70.31B end of 2015, and reach $71.21B end of February 2016. On the monetary front, BDL’s total assets grew 4.04% y-t-d to $94.58B end of Q1 2016. Gold reserves grew 15.56% to $11.38B, while foreign assets ticked down 1.35% to $36.59B by March 2016. The growth in gold reserves resulted from the 16.12% increase in gold prices in the first 3 months of 2016. As for total assets at commercial banks, they grew by 0.32% y-t-d to $186.59B by January 2016. On the Beirut Stock Exchange, investors started the year with optimism, as shown by the BLOM Stock Index (BSI) that added 1.28% q-o-q, to 1,184.49 points end of March. Trade volume surged from 231,158 shares worth $2.12M, in Q4 2015 to 30,998,231 shares worth $278.51M in Q1 2015. As for market capitalization, it broadened by $60.55M since year-start, to $9.79B end of Q1 2016.