The juridical decision regarding Husni Mubarak, and the Jihadists attacks in Sinai, were the two main events that marked the last quarter of 2014. Jihadist attacks in Sinai targeting Egyptian militaries killed 31 soldiers in October forcing President Al-Sisi to declare a 3-month state of emergency in the Peninsula. Measures, to prevent weapons’ smuggling, were also initiated such as demolishing residences along Gaza border to build a 500-meter buffer zone.

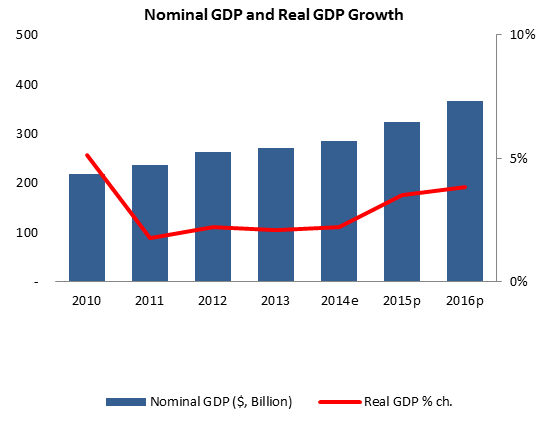

The clampdown in the Egyptian security situation failed to hinder the economic performance of the country. Focusing on economic growth and fiscal reforms, Egypt registered, in the first quarter of the financial year (FY) 2014/15, its highest yearly growth since Q4 2007/08. According to Official sources, real Gross Domestic Product (GDP) has risen at a rate of 6.8% between July and September mainly on improving activity in the manufacturing and tourism industries.

In the same context, the International Monetary Fund (IMF) held, in November 2014, Article IV consultations, for the first time in 4 years. Once the mission was concluded, the IMF projected economic growth to reach 3.8% in FY 2014/15 and set suitable economic goals, of which boosting growth and gradually soothing inflation. When it comes to prices, annual inflation reached 10.13% in December 2014 compared to 9.09% in the previous month and 11.66% in June 2014.

On another front, tourism activity managed to post positive performance in the first ten months of 2014. This was mainly due to the election of President Al Sisi, the relatively controlled security situation and the lift of some European flights halts to Egypt. Correspondingly, the overall tourists’ number improved by October 2014 adding 1.1% y-o-y to 8.20M. Worth mentioning that October alone saw more than 1M tourists, an 18-month high. This was directly reflected on tourism revenues which more than doubled in Q1 of FY 2014/15 to settle at $2.1B against $931.1M in the same period of 2013.

The mounting tourism revenues can be explained by the progressing occupancy rate in Cairo’s hotels as it inched up by an average of 9 percentage points (p.p) to 35% in 2014 compared to 25% in the first eleven months of 2013. In the same context, the average room rates rose 11.8% y-o-y to settle at $92, while room yields surged 47.2% y-o-y to $31 by the end of November 2014.

On the external level, the Balance of Payments recorded, in the first quarter of FY 2014/15, a surplus of $410.0M however lower than the $3.7B registered a year earlier. The surplus tightening was mostly due to the substantial slump in the country’s current account balance that sank into a deficit of $1.44B by Q1 FY 2014/15 from a surplus of $609.6M a year ago. The latter was severely impacted by the 29.2% y-o-y broadening of Egypt’s trade deficit that reached $9.74B during July/Sept of FY 2014/2015 on higher merchandises imports.

On the brighter side, net inflow of Foreign Direct Investments (FDI) edged up from $745.4M to $1.8B during the period under review on higher net inflow from the oil sector and Greenfield investments. To note here that Egyptians working abroad highly boosted remittances to the country as they surged by 16.6% y-o-y to $4.71B in Q1 FY2014/2015.

Concerning the country’s fiscal position, and considering the government’s fiscal reforms, the IMF estimated budget deficit to reach 11% of GDP for FY 2014/15. However, the first quarter of the FY 2014/15 revealed a broadening fiscal deficit (including net acquisition of financial assets) of $8.84B compared to the $8.05B recorded in Q1 FY 2013/2014. In details, the overall revenues surged 30.3% y-o-y to $10.27B over the mentioned period, while total fiscal expenses followed at a slower pace of 20.3% to $18.94B. Regarding the nation’s debt, it stood at $247.14B by the end of September 2014 compared to $214.18B in September 2013.

However, the country’s international standing has improved with Fitch upgrading Egypt to “B” from “B-“ with stable outlooks in early January 2015. On another note, the Egyptian authorities are foreseeing, for the first time in the country’s history, a Eurobonds issuance worth $1.5B aiming to attract influx of new foreign capitals.

The monetary standing of Egypt was highly dependent on the worldwide economic developments related to the drop in oil prices, the Eurozone challenges and the tempering growth in emerging markets along with the internal reforms initiated by Al Sisi. Hence, Egypt’s Central Bank (ECB) initiated new measures alluding to a probable shift in monetary policy from anchoring inflation to boosting growth. In fact, the Monetary Policy Committee (MPC) decided to cut levels of interest rates by mid-January 2015 in order to stabilize risks surrounding the inflation and GDP outlooks. In the same context, ECB’s key interest rates were cut by 50 basis points to 8.75% for the overnight deposit rate, 9.75% for the overnight lending rate and 9.25% for the discount rate. Similarly, and aiming to reduce the gap between the official exchange rate and the black market rate, the ECB also permitted the Egyptian pound’s depreciation through its FX auctions, for the first time since May 2014, with the exchange rate going from EGP7.15/USD to EGP7.40/USD.

When it comes to monetary indicators, net foreign reserves slumped from $17.03B in 2013 to end 2014 at $15.33B. Confidence in the banking sector’s resiliency bolstered total deposits (including government deposits) by 18.5% y-o-y to $201.09B in October 2014, and total lending activity by 12.0% y-o-y to $82.26B.

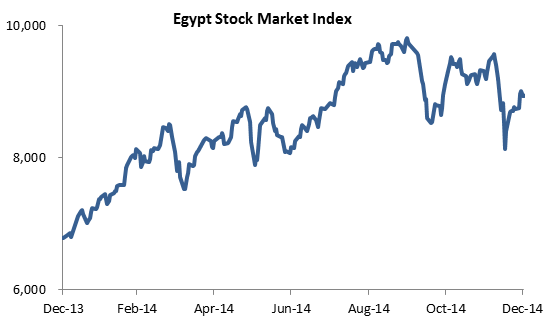

The Egyptian stock exchange ended 2014 in the green and showed strength despite the country’s circumstances and the newly imposed taxes on distributed dividends and capital gains. Hence, investors’ high interest that overrode the new rules with the EGX30 surging by an annual 31.6% to 8,927 points by the end of 2014. The average daily volume traded reached 195.52M shares worth $96.83M in Q4 2014, up from 153.50M shares worth $69.53M recorded a year earlier. Market capitalization stood at $69.32B up from $61.91B in December 2013 with the number of transactions increasing by a yearly 20.4% to 1.74M.