The drop in the registered number of Syrian refugees served to reduce pressure on the Jordanian Kingdom and allowed for a positive outlook for 2015. In fact, the UNHCR expected the number of Syrian refugees (by December 2014) to stand above 800,000, while the actual number reached was 747,360, as entry to Jordan through Syria’s southern border became less probable for refugees due to harsher conditions and confrontations.

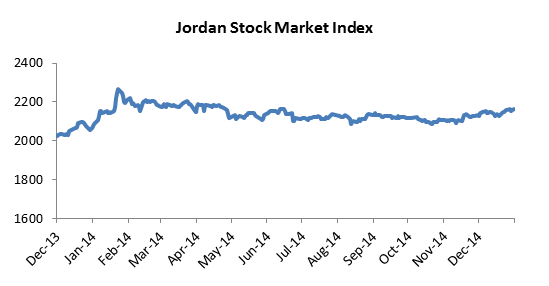

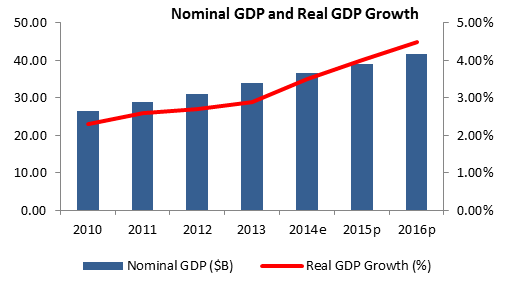

In parallel, Jordan managed to continue its strong development programs built on foreign aid, as the $1B Overseas Private Investment Corporation’s (OPIC) investments covered areas ranging from education and health services to renewable energy and power, while a $250M aid agreement with USAID in October aimed to stimulate economic growth and help restore fiscal balance. On the economic front, the International Monetary Fund (IMF) anticipated growth rate to reach 3.5% in 2014, up from 2.9% in 2013, while the inflation rate for 2014 stood at 3.0%, with the largest increases in the CPI observed in the clothing and footwear index, followed by real estate and housing. Jordan’s tourism sector continued its improvement by November 2014, as tourism receipts progressed by $250.00M year-on-year (y-o-y) to $3.34B. Part of these revenues can be attached to important religious events that took place throughout the year, with the visit of Pope Francis in end-May a key contributor. Likewise, the number of tourists by end-September revealed a 0.5% y-o-y uptick to 4,155,724. Meanwhile, Ernst & Young’s hotel occupancy report displayed a marginal downtick in Amman’s occupancy rate by November 2014 to 60.0% compared to the previous year’s 62.0%. On the external front, Jordan’s trade deficit widened by 3.37% y-o-y in the first eleven months of 2014 to $14.79B, as the 6.28% y-o-y increase in exports failed to compensate for the 4.25% yearly jump in imports. The increase in imports came as a result of increased energy imports from Russia, India and the UAE to replace imports from Egypt, which declined by 20.24% due to disruptions in gas supplies. Meanwhile, the broadening of exports resulted from the progress in exports of crude phosphates in addition to clothing accessories, which respectively increased by 15.75% y-o-y and 12.34% y-o-y. Jordan posted an improved performance regarding the fiscal deficit and continued to be in line with IMF requirements. The fiscal deficit (including foreign grants) dropped 22.45% y-o-y by end-October 2014 to stand at $980.28M. Simultaneously, net public debt remained at 80% of GDP as net outstanding domestic and external debt rose by $1,016.90M and $919.58M to reach 49.2% and 30.8% of GDP, respectively. Jordan’s general budget displayed a primary surplus, which excludes interest payments, equal to $121.13M, an improvement on the $432.96M primary deficit posted by October 2013. Accordingly, Jordan’s S&P rating stood at stable despite the regional problems the Kingdom faced. This also allowed for the completion of the IMF’s fifth review of its Stand-By Arrangement, which cleared the disbursement of $125.4M on November 10th, bringing the total amount granted by the IMF in their $2B agreement to $1.38B. Noteworthy improvements were seen in Jordan’s banking sector during the last quarter of 2014 in spite of the continuing deterioration of regional conditions on the political and security fronts. In details, money supply M2 revealed a 5.11% y-o-y uptick to $41.20B by November 2014, while total credit facilities revealed a 3.74% y-o-y rise to $27.48B as of end-November 2014. This uptick was influenced by the 7.45% and 3.17% annual increases in facilities denominated in foreign and local currencies to respective values of $3.91B and $23.58B by November 2014. Total deposits held with banks also swelled by 9.49% y-o-y to $42.63B by November 2014. Deposits denominated in Jordanian Dinar (JD) jumped 14.04% y-o-y to a value of $33.67B by November 2014 which was slightly offset by the 4.79% y-o-y dip in foreign currency deposits to $8.96B during the same period. To maintain the recovery of its economy, the Central Bank of Jordan held two key monetary policy instruments at their current levels, namely the overnight deposit window facility and weekly repurchase agreements rates, which remained at 2.75% since May 2014 and 4.00% since January 2014, respectively. The Amman Stock Exchange (ASE) ended 2014 on a positive note, and performed well in the face of regional turbulence with its impact on the political front and in the face of a significant drop in oil prices with its impact on the economic front. The ASE, as of end-December 2014, posted a y-o-y increase of 4.82% to 2,165.46 points. In detail, 634.11M shares traded in Q4 2014 for a total traded value of $775.34M, a 4.27% y-o-y rise. Similarly, the total number of trading transactions augmented 3.93% to 241,513. Meanwhile, the market capitalization for the fourth quarter of 2014 stood at $26.51B, a 0.83% y-o-y downtick as increased prices were offset by 7 de-listings on the ASE during 2014.