With no president of the republic being elected since the 25th of May, the Lebanese Parliament extended its mandate by 2 years and 7 months, in November. However, this extension was coupled with a law stating that parliamentary elections would occur after the presidential election.

With no president of the republic being elected since the 25th of May, the Lebanese Parliament extended its mandate by 2 years and 7 months, in November. However, this extension was coupled with a law stating that parliamentary elections would occur after the presidential election.

The security situation remained shaky, as Lebanon continued suffering from the Syrian civil war spill-over effects. 4 bombings occurred in the fourth quarter (Q4) 2014, 3 of which were in Arsal, while the fourth in eastern Lebanon.

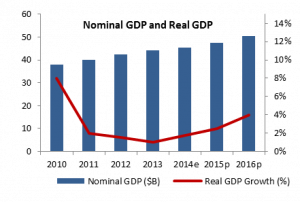

Despite the political and security upheavals that Lebanon had faced during 2014, economic growth rate managed to increase slightly from 1.50% in 2013 to 1.75% in 2014. Furthermore, the BLOM Purchasing Manager Index stood at an average of 49.2 points in the last quarter (Q4) of 2014, compared to an average of 47 points in the third quarter (Q3), however still below the 50 mark.

Low international energy prices triggered a 0.71% y-o-y deflation, with the Consumer Price Index standing at 99.29 points, end of 2014. “Water, electricity, gas and other fuels” sub-index and “transportation” sub-index recorded yearly declines of 8.92% and 8.46%, respectively.

As for the real estate sector, it witnessed a quarterly improvement, where transactions jumped 6.18% compared to Q3, to 18,891. Foreigners showed more confidence in Lebanon, where their share increased from 1.57% in Q3 to 2.15% in Q4.

In contrast, the stagnating economy weighed down on construction, with the number of permits declining 5.50% q-o-q to 3,830. Moreover, new projects experienced a downsizing, where the construction area authorized by permits shrank 1.20% compared to the previous quarter, reaching 2.99M sqm in Q4.

Then again, tourism saw a yearly improvement of 6.30% in 2014 to 1,354,647 tourists. This could be attributed to the low base reached in 2013 in more than 8 years. The main incomers were Arabs and Europeans that increased 14.61% and 3.15%, respectively. Similarly, hotel occupancy experienced a slight progress, with the average rate adding 1 percentage point to 51% by November. Nevertheless, this came at the back of lower profits, where the average room rate and average room yield lost 3.31% and 1.60% to $162 and $84, respectively.

Lebanon recorded a deficit of $1.29B on its balance of payments by November 2014, compared to a larger deficit of $1.66B during the same period in 2013.

The tightening in the deficit could be partly attributed to improving capital inflows and remittances from the Lebanese expatriates, and the 0.64% y-o-y narrowing in trade deficit, to $17.19B in 2014. Imports displayed a 3.47% decline to $20.49B, while exports dropped by 15.95% to $3.31B end of 2014. Worth noting that Foreign Minister, Gebran Bassil, signed a free-trade agreement with the Mercosur countries of Latin America, aiming at maintaining good relations with the bloc, and facilitating trade between Lebanon and these countries.

Shifting to the fiscal sector, gross public debt climbed 5.33% y-o-y to reach $66.63B, in the first 11 months of 2014. In contrast, fiscal deficit narrowed 32.46% yearly to $2.22B in the first 3 quarters of the year, whit a primary surplus of $867M compared to a primary deficit of $546M, during the same period last year. This progress came as a result of a 12.57% increase in total revenues coupled with a 1.79% drop in total expenditures. The rise in revenues was driven by a strong recovery in revenues from telecom (5.22%) and VAT (0.93%), while the main decrease in expenditures came as a result of the 11.53% decline in transfers to Electricite du Liban, owing to the fall in international oil prices. Moreover, to meet its foreign currency needs in the coming years, the Parliament authorized the issuance of $2.42B in new Eurobonds by the Ministry of Finance.

The monetary front remained hale and hearty, as BDL’s total assets edged up 0.31% q-o-q, to stand at $85.70B by the end of 2014. However, its foreign currency reserves lost 1.46% during the same period to $37.86B, but still remained at a very high level. Total assets of commercial banks posted a 4.48% increase since year start, to $172.21B by November.

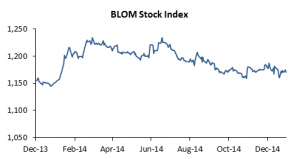

Political and security developments continued to distress investor sentiment on the Beirut Stock Exchange. The BLOM Stock Index (BSI) dropped a marginal 0.33% since last quarter, to 1,170.26 points end of December, 2014. Trade occurred at a lower average volume of 295,446 shares worth $2,003,389 compared to that of the previous quarter of 740,344 shares worth $4,671,764. Market capitalization widened from $9.71B to $9.78B, following the listing of 4.76M Bank of Beirut Priority shares on the BSE in October.