Mega projects kept on labeling the United Arab Emirates’ strategy to establish itself as a regional financial center and a hub for transport, tourism and trade. In fact, Dubai, being the host of the World Expo 2020 is planning to spend $6.80B on related infrastructure which includes the extension of the Dubai Metro. Also, and as part of the GCC rail network, Abu Dhabi will spend $10.9B on the Etihad Rail link project. In details, the Emirate’s project stretches over 1,200 km from the Saudi border to the Omani border in the south of Fujairah.

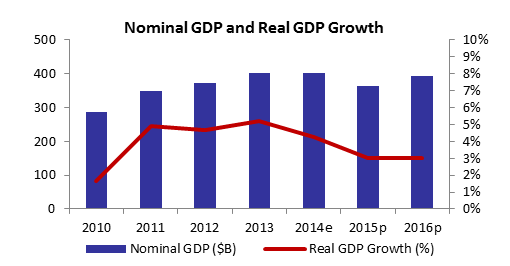

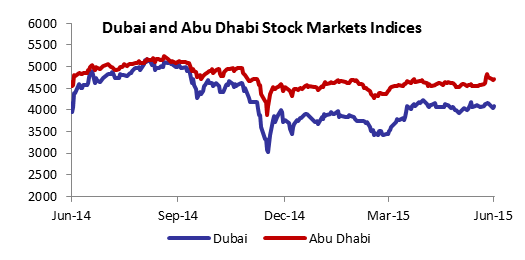

Economic data showed that business conditions in the UAE’s non-oil private-sector economy continued to improve during the second quarter of 2015. The International Monetary Fund (IMF) expects UAE’s real Gross Domestic Product (GDP) to grow by 3.15% in 2015 and by 3.16% in 2016. Moreover, the UAE’s Purchasing Managers’ Index (PMI), which illustrates the performance of the non-oil producing private sector in the UAE, slowed down from 58.20 in June 2014 to 54.70 in June 2015. However, the rate of business expansion remains strong and the country is setting to continue to perform strongly amid a favorable business environment and a progress in government spending which will help the economy go forward and become less vulnerable to oil price fluctuations. Looking at inflation for the two main Emirates, the Consumer Price Index (CPI) in Abu Dhabi rose by 5.28% y-o-y whereas Dubai’s CPI increased by 4.68% y-o-y from May 2014 to May 2015 due to a rise in prices of “Housing”, “Furnishing & Housing equipment”, “Beverages & Tobacco” and “Education” in both emirates. Tourism in Dubai sustained its quick ascent during the second quarter of 2015. Dubai International Airport (DXB) saw the number of passengers reach a record level of 32.38M for the first five months of 2015, a 9.38% yearly increase over the same period. Moreover, according to Ernst & Young hotel benchmark survey report, Dubai hotels maintained their top ranking amongst the Middle East and North Africa (MENA) countries in terms of occupancy rate at 86.0% by May 2015 preserving the same level of the similar period of 2014. Abu Dhabi came second with an 81.0% hotel occupancy rate, one percentage point lower than the same period in 2014. In contrast, the Emirates’ external performance showed signs of weakness over the past six month of 2015. In fact, the Institute of International Finance (IIF) expected the current account balance to fall by 73.14% y-o-y by the end of 2015 to $13.10B. This can be accredited to the 29.74% annual contraction in the trade balance from $114.70B in 2014 to $80.60B in 2015 which in turn can be linked to lower international oil prices from Mid-2014 up until now. This downturn in global oil price had a direct impact on the Emirates’ hydrocarbon exports which dropped by 41.52% y-o-y from $110.10B in 2014 to $64.40B in 2015. On the non-hydrocarbon export side, a 4.00% increase to $266.20B in 2015 is forecasted following the Emirates persistent effort to diversify away from oil. Total imports over the period were also expected to decline by 0.56% y-o-y from $251.40B in 2014 to $250.00B in 2015. Consequently, and in line with the bearish oil prices trend, the UAE’s fiscal balance is expected to witness a radical shift and register a deficit of $13.32B in 2015 y-o-y down from a surplus of $28.84B. In details, consolidated revenues are estimated to decrease by 29.41% y-o-y from $132.77B in 2014 to $93.72B at the end of 2015. This will mostly result from a 40.82% expected slump in hydrocarbon revenues. However, non-hydrocarbon returns are expected to increase from $30.78B in 2014 to $33.36B in 2015. On the spending level, consolidated expenditures (excluding net lending) are forecasted to increase by 3.00% up from $103.92B in 2014 to $107.04B in 2015. Monetary developments reflected the robust economic performance of the Emirates. In details, M3 increased by 2.20% during the first quarter of 2015 and by 6.60% y-o-y to $375.24B. Total bank assets rose by 7.10% y-o-y to $650.99B in May 2015 up from $607.95B in May 2014. This hike was brought about by a 7.94% y-o-y increase in credit, reaching $389.94B by May 2015 compared to $361.16B in May 2014. Total bank deposits (resident and non-resident customers) increased by 4.78% to $393.80B in May 2015, compared to $375.81B in May 2014. In specifics, the yearly 3.80% progress to $354.44B in total resident deposits was outpaced by the 14.40% increase to $39.37B in total non-residents deposits in May 2015. Positive Q1 results for companies in the financial and real estate sector were probably the main aids on trading activity of Dubai and Abu Dhabi’s stock markets. This was translated into the indices of both financial stock markets (Dubai and Abu Dhabi) experiencing respective 16.29% and 5.71% q-o-q improvements to 4,086.83 points and 4,723.23 points by end of June 2015. Accordingly, Dubai and Abu Dhabi’s market cap broadened by respective amounts of 14.16% and 6.39% from Q1 reaching $97.76B and $120.26B. In terms of trading activity, Dubai’s financial market average daily traded volume widened by 39.98% q-o-q to 535.06M shares in Q2 2015 at an average traded value of $235.84M (compared to an average daily traded volume of 382.25M shares worth $165.29M in Q1 2015). Similarly, the number of transactions progressed to 499,423, up from 388,732 recorded last quarter. Abu Dhabi experienced similar market dynamics, as the average daily volume surged by 41.49% q-o-q to 121.28M shares worth $64.15M in Q2 2015 compared to 85.72M stocks valued at $58.36M in Q1 2015. As for the number of transactions, it tallied to 115,322 by End-June 2015, higher than the 107,256 transactions registered in last quarter.