Lebanese Banks Require BDL Approval to Sell/Buy Assets in Local Dollars; Total Assets Down to $102.87B in February 2025

BDL issued on April 14th, 2025 intermediate circular #734 (decision 13717) amending some of the clauses mentioned in the previous intermediate circular #733 (decision 13716) related to restrictions on banks’ operations. In details, this new circular requires banks to get a prior approval from the Central Bank before trading of stock listed on Beirut Stock Exchange, Eurobonds and other securities in local dollars. Moreover, the circular cancelled the clause that states that banks should take a prior approval to sell Eurobonds abroad.

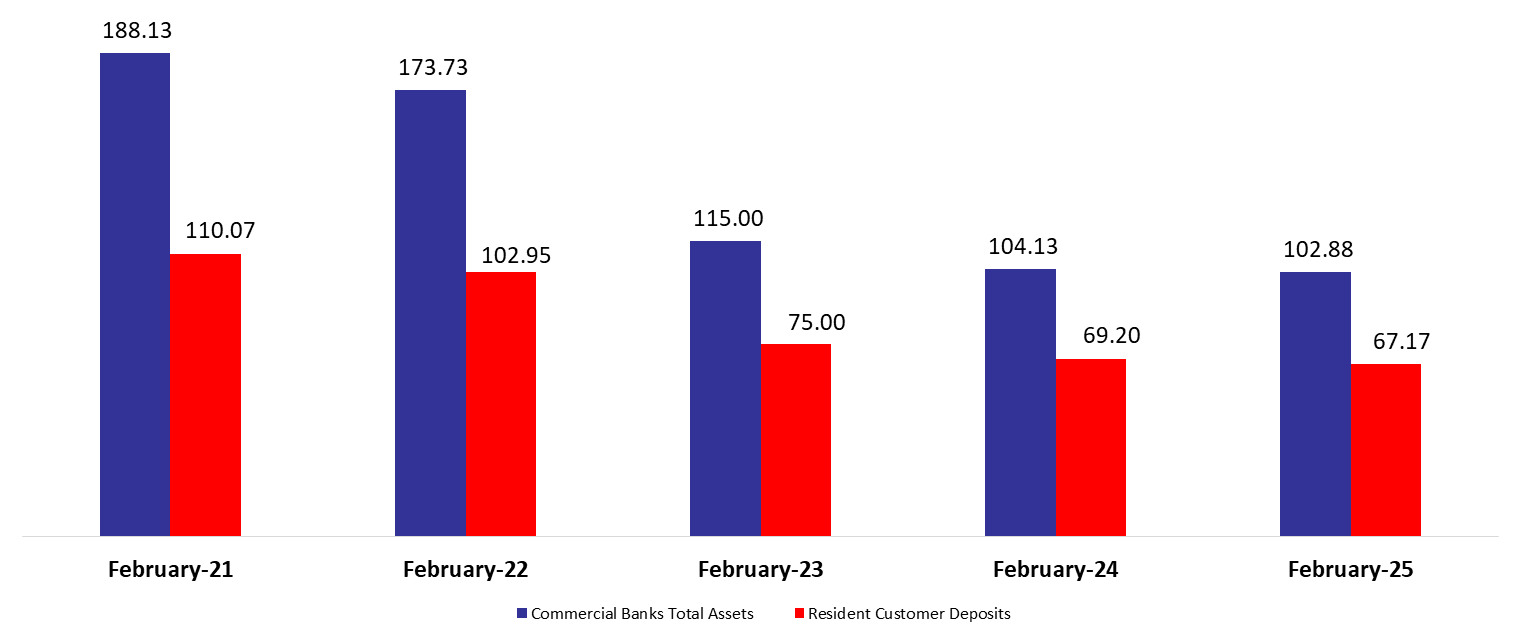

According to Lebanon’s consolidated commercial banks’ balance sheet, total assets declined by 1.20% on year over year (YoY) basis to stand at $102.87B in February 2025 amid BDL’s adoption of a new exchange rate of LBP 89,500 per USD effective 31/01/2024.

On the assets side, currency and deposits with Central Bank represented a high figure of 77.10% of total assets; they dropped annually by 2.38% to settle at $79.32B in February 2025. Deposits with the central bank (BDL) represented 99.89% of total reserves, and decreased by 2.37% YoY, to reach $79.23B in February 2025. Furthermore, vault cash in Lebanese pound declined by 10.35% on a yearly basis to stand at $85.04M by the same period.

Claims on resident customers, constituting 4.60% of total assets, shrank by 22.19% to stand at $4.74B in February 2025. Moreover, resident securities portfolio, representing 5.87% of total assets, increased by 26.27% in February 2025 to stand at $6.04B. More specifically, the Eurobond holding recorded an increase of 12.59% since February 2024, to reach $2.47B (net of provisions) in February 2025. Additionally, claims on non-resident financial sector rose by 15.42% YoY to stand at $5.04B by February 2025.

On the liabilities side, resident customers’ deposits were the main account, representing 65.29% of total liabilities; they dropped by 2.94% since February 2024 to reach $67.16B by the month of February 2025. In more details, deposits in foreign currencies (being 98.81% of resident customers’ deposits) declined by 3.37% YoY to reach $66.36B by February 2025, additionally deposits in LBP (1.19% of resident customers’ deposits) increased by 52.57% YoY to stand at $800.26M by February 2025. This reveals that a slightly higher proportion of deposits are now held in LBP, as the dollarization ratio for private sector deposits decreased from 99.37% in February 2024 to 99.03% in February 2025.

As for non-resident customers’ deposits, grasping 20.35% of total liabilities, they recorded a drop of 0.10% and stood at $20.94B in February 2025. In details, the deposits in LBP rose by 0.53% to reach $31.50M and deposits in foreign currencies declined by 0.11% to reach $20.91B over the same period. In addition, non-resident financial sector liabilities representing 2.47% of total liabilities and decreased by 6.95% YoY to reach $2.54B in February 2025.

Lastly, the capital accounts stood at $4.63B, higher by 45.83% than February 2024, noting that only about 10% of those are in LBP.

Commercial Banks Total Assets and Resident Customer Deposits in February 2025 ($B)

Source: BDL, BLOMINVEST

Disclaimer:

This article is a research document that is owned and published by BLOMINVEST BANK SAL.

No material from this publication may be modified, copied, reproduced, repackaged, republished, circulated, transmitted or redistributed directly or indirectly, in whole or in any part, without the prior written authorization of BLOMINVEST BANK SAL.

The information and opinions contained in this document have been compiled from or arrived at in good faith from sources deemed reliable. Neither BLOMINVEST BANK SAL, nor any of its subsidiaries or affiliates or parent company will make any representation or warranty to the accuracy or completeness of the information contained herein.

Neither the information nor any opinion expressed in this research article constitutes an offer or a recommendation to buy or sell any assets or securities, or to provide investment advice.

This research article is prepared for general circulation and is circulated for general information only.