Pressure on the Hashemite Kingdom of Jordan continued to ease with the decreasing number of Syrian refugees. The UNHCR had previously estimated the number to increase over 2015 from 811,070 to above the 1M-mark, only for the total number to currently stand at 628,427 as it became more difficult for Syrians to cross the border in to Jordan. Despite this alleviation of duty, Jordan has only received 8% of the required $1.19B in aid needed to help the refugees, resulting in the opening of discussions with the U.S on an aid package. The Kingdom is also attempting to begin work on an $18B crude oil pipeline between Basra and Aqaba in coordination with the Iraqi government. The Kingdom’s economic performance was also hindered by the execution of the military pilot Kassabeh on February 3 and the Kingdom’s consequent participation in air raids against the Islamic State.

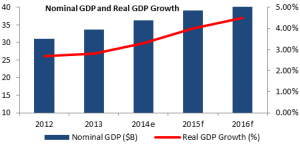

On the economic front, the International Monetary Fund (IMF) concluded its sixth review under its 2-year standby arrangement with Jordan, resulting in the allowance of the distribution of $200M in aid. Also, the IMF expected growth rates to hover near the 4% mark in the near future (3.8% in 2015 and 4.5% in 2016), and forecasted inflation to stand at 1.2% during the year due to lower commodity prices as consumer prices dropped only 0.2% during January 2015. On the economic front, the International Monetary Fund (IMF) anticipated growth rate to reach 3.5% in 2014, up from 2.9% in 2013, while the inflation rate for 2014 stood at 3.0%, with the largest increases in the CPI observed in the clothing and footwear index, followed by real estate and housing. Jordan’s tourism sector experienced a poor start in 2015, as the Kingdom failed to build on an improved industry in the previous year. The reduced performance is linked to the increased contribution of the Kingdom to airstrikes against the Islamic State following the execution of a Jordanian military pilot. Consequently, travel receipts for January 2015 displayed a 6.0% y-o-y downtick to $345.88M. In addition, tourist arrivals for the first two months of 2015 stood below the 1M mark, at roughly 997,300 tourists, representing an 8.02% annual decline. Furthermore, Ernst & Young’s hotel occupancy report displayed a 12 percentage-point (pp) y-o-y drop in Amman’s occupancy rate to 46%, while the average room yield also decreased over the same period by 20.1% to $73 per room. On the external front, Jordan’s trade deficit narrowed by 16.90% y-o-y by end-February 2015 to $1.84B. This contraction was due to the decrease in the Kingdom’s imports outpacing that of the exports. Despite the Egyptian gas supply cuts, imports during the first 2 months of 2015 managed to slump by 15.52% to $2.98B. This was mainly due to the global plummet in oil prices that offset the Kingdom’s needs for greater imports of energy from Russia, UAE and India. In parallel, total exports by February 2015 suffered a slighter dip of 13.18% in value to $1.14B on the back of reduced export of minerals and chemical fertilizers, in addition to crude and phosphates by 45.35% and 17.49%, respectively. Jordan continued to improve on its fiscal performance and remain in line with its IMF obligations. Jordan’s S&P rating remained stable, and allowed for the successful completion of the IMF’s sixth review of the $2B standby arrangement. Consequently, the fiscal deficit, including foreign grants, narrowed by 18.25% y-o-y to $1.27B. In parallel, Jordan’s net public debt attained 80.9% of GDP as a result of an 8.42% annual growth to $29.23B, as outstanding domestic (49.5% of GDP) and external debt (31.4% of GDP) up-ticked by $1.13B and $1.14B, respectively. Meanwhile, the Kingdom’s general budget displayed a slight primary deficit of $54.21M by November 2014, which excludes interest payments amounting to $1,216.62M, a marked improvement on the $617.73M deficit of the previous year. Jordan’s banking sector continued to post improved performances in 2015 despite local and regional struggles. Specifically, money supply M2 augmented 6.93% y-o-y to stand at $41.91B by January 2015. Similarly, total credit facilities rose 1.63% annually to $27.25B over the same period. This increase is explained by facilities denominated in local currency improving 5.01% y-o-y to $24.47B by January, with facilities denominated in foreign currency declining by 20.94% y-o-y to $2.78B. Moreover, total deposits at licensed banks were boosted by 9.81% y-o-y to $43.49B at end-January. In details, deposits denominated in local currency gained an annual 13.82% to $34.62B, while deposits in foreign currencies contrastingly decreased by 3.46% y-o-y to $8.88B. It is also worth mentioning that 79.07% of total deposits were made by the resident private sector, down from 80.26% at the same time last year. On the 3rd of February, 2015, the Central Bank of Jordan drove down two main monetary policy tools in a bid to boost economic activity across all economic sectors and improve banking liquidity, as the overnight deposit window rate and the weekly repurchase agreements rate dropped from 2.75% and 4.00% in January 2015 to respective levels of 1.75% and 2.75%. The Amman Stock Exchange (ASE) posted a mixed beginning to 2015, with Q1 performance split in to two trends. Between January 1st and February 3rd, the Jordanian bourse posted a 3.30% increase on the back of improved IMF expectations for inflation and growth. However, the positive performance that depicted the first month was overshadowed by Kassabeh’s execution. Accordingly, the ASE experienced a slump in performance resulting in an overall y-t-d decline of 1.39% to 2,135.43 points. In detail, 464.18M shares were traded during the first three months of 2015 for a combined worth of $732.08M, compared to 473.50M shares worth $786.51M during the first three months of 2014. In parallel, total market capitalization at the end of Q1 2015 stood at $24.23B while total transactions added up to 61,193, posting respective downticks of 11.41% and 4.05% y-o-y.